Solana just gave delegators a new governance tool called Solana Governance Proposals (SGP), which hands them a lever for the next round of the inflation fight.

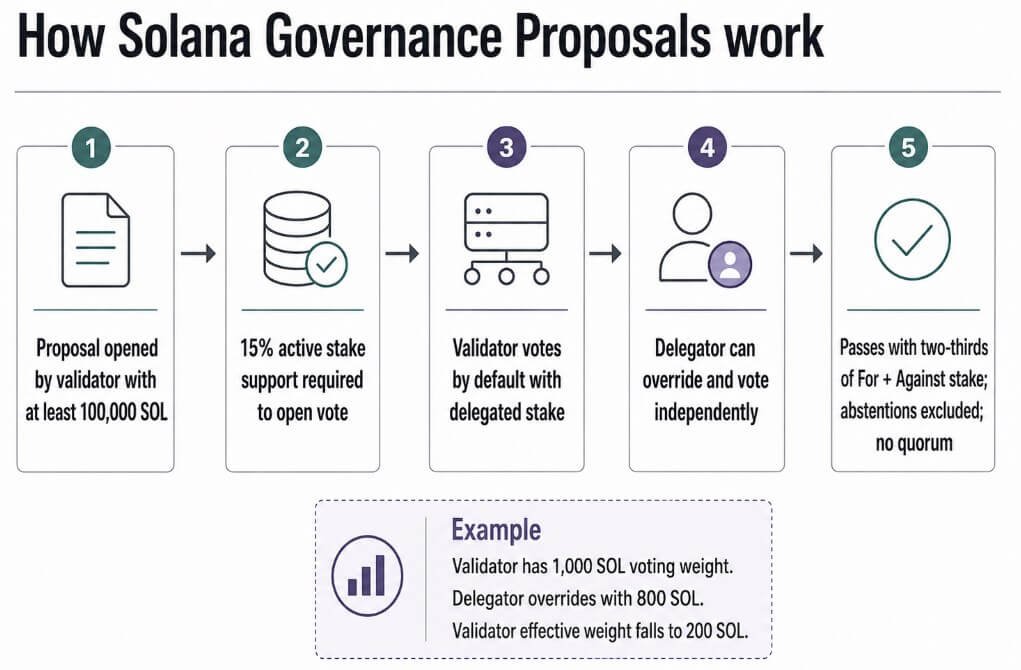

The proposing validator’s vote account must have at least 100,000 SOL staked, worth about $7.8 million at $77.97 per token. To advance from proposal to vote, validators representing 15% of Solana’s active stake must support it. Based on 428.1 million SOL in active stake, that threshold is roughly 64.2 million SOL, worth close to $5 billion.

By default, a validator votes with the SOL delegated to its vote account, but a delegator can deviate from that default and vote independently.

Take a validator vote account with 1,000 SOL in stake, including 800 SOL delegated by a single staker. If that delegator submits an independent vote, the 800 SOL moves out of the validator’s tally and into whatever the delegator chose: For, Against, or Abstain, leaving the validator with just 200 SOL of effective weight.

Multiply that across custodians, stake pools, and exchanges holding SOL on behalf of thousands of depositors, and a validator’s assumed voting bloc can end up far smaller than its delegated total.

A proposal passes only if ‘For’ votes represent at least two-thirds of the stake that votes either ‘For’ or ‘Against.’ Abstentions are excluded from that calculation, and there is no separate quorum requirement.

The SIMD-0228 precedent

That 66% bar is where the last major inflation fight fell short: Multicoin Capital’s Tushar Jain and Vishal Kankani authored SIMD-0228proposing to tie SOL issuance to staking participation and to cut emissions once the network reached a well-secured level.

It drew 61.39% approval against a 66.67% requirement, even as roughly 74% of staked SOL weighed in, a turnout that ruled out any low-stakes formality.

Validators staking 500,000 SOL or less voted against SIMD-0228 over 60% of the time, while larger operators leaned the other way.

Treating the SIMD-0228 result as 100 units of decisive stake, split 61.39 For to 38.61 Against: flipping just 5.28 of those points from Against to For clears 66%. Reclassifying 7.92 points as abstain does the same job, since abstentions drop out of the denominator entirely.

Bringing in fresh stake that never voted at all takes more, about 15.84 new For units for every 100 old ones.

| Path to clearing 66.67% | What changes | Minimum shift needed | Why it matters |

|---|---|---|---|

| Flip Against to For | Some prior Against stake becomes For | 5.28 points | Smallest swing needed |

| Move Against to Abstain | Some Against stake exits the denominator | 7.92 points | Abstentions do not count toward approval threshold |

| Add new For voters | Previously inactive stake votes For | 15.84 new For units per 100 decisive units | Harder because total voting stake rises too |

| Scale marker today | 5.28-point swing applied to today’s active stake and prior turnout | ~16.8M SOL / ~$1.3B | Shows the margin was economically large but governably narrow |

Scaled against today’s 428.1 million SOL in active stake and the 74% turnout from the prior vote, that 5.28-point swing works out to roughly 16.8 million SOL. At current pricesthat’s about $1.3 billion.

The model treats the prior vote as a fixed baseline and measures the distance from the threshold, a rough gauge of how tight the actual margin was.

Solana’s inflation schedule started at 8% a year, cuts by 15% annually, and targets a 1.5% floor in the long term, with third-party trackers putting the live rate near 3.76% today.

That number touches staking yield, validator revenue, dilution for every SOL holder, and the security budget that keeps the network running.

The Federal Reserve held the federal funds target range at 3.50% to 3.75% at its June 17 meeting, and FRED listed the upper bound unchanged at 3.75% as of July 2.

A SOL holder weighing staking yield against parking cash elsewhere runs the math whether or not Solana’s governance page accounts for it.

Two ways this goes

The bull case for SOL holders runs through the delegators who are most equipped to act. Custodians, stake pools, exchanges, and large native holders can track proposals, execute votes at scale, and withdraw stake from validators who vote ‘Against.’

If enough of them act after a fresh emissions proposal clears the 15% support gate, a SIMD-0228-style cut has a more plausible path to the 66.67% approval threshold, whether the new terms are stricter or softer than the original.

Lower issuance reduces dilution and limits the extra SOL entering the market with every new token minted. Solana’s governance is starting to look like something SOL holders steer directly.

The bear case plays out through inaction, with no validator coalition reaching 15% support for an aggressive cut. Alternatively, a vote opens, and override turnout stays thin because staking interfaces don’t make participation easy, custodians skip building the tooling, or delegators skip voting.

Validator revenue sits where it sat before SGP existed, and the next inflation fix waits for whatever vote comes next.

| Scenario | What has to happen | Who gains influence | What happens to inflation reform |

|---|---|---|---|

| Bull case for SOL holders | A new emissions proposal clears the 15% validator support gate, and large delegators actively override validator votes | Custodians, stake pools, exchanges, institutions, large native stakers | A SIMD-0228-style cut has a clearer path to passing |

| Bear case for reform | No validator coalition reaches 15% support, or override turnout is weak | Validators retain practical control over delegated stake | Inflation reform stalls or returns in a softer form |

| Validator-protection case | Smaller operators successfully argue that issuance cuts threaten decentralization and security economics | Long-tail validators, operators dependent on staking rewards | Any cut is phased, capped, or paired with other revenue assumptions |

| Governance-risk case | Overrides are used mostly by whales, custodians, or exchanges rather than broad retail delegators | Large stake controllers | Governance becomes less validator-dominated but not necessarily more decentralized |

Smaller validators make a real economic case: issuance funds the network’s security budget as much as it dilutes holders.

Cutting it compresses the yield that keeps thin-margin operators solvent, pushing stake toward larger validators with other revenue streams already in place.

Helius’ review of SIMD-0228 pointed to the same problem from a different angle, tying long-tail validator economics to voting costs, block rewards, MEV, and commission structures, alongside inflation.

Validators vote with the stake they don’t own outright, and the cost of high issuance lands on every SOL holder regardless of who they staked with.

SGPs give delegators a direct way to separate their own preference from their validator’s default when an issuance proposal reaches a vote.

SGPs redraw who gets counted the next time issuance reaches a vote. Getting the number down still takes a proposal that clears both gates and a delegator base willing to act once it does.

Validators lost the assumption that every SOL staked with them will vote the way they do.