Strategy reported a massive first-quarter loss after Bitcoin’s early-year drawdown overwhelmed its software revenue, even as Michael Saylor pointed to internal Bitcoin metrics showing continued gains in shareholder exposure.

The company, formerly known as MicroStrategy, reported a net loss attributable to common stockholders of $12.77 billion, or $38.25 per diluted share, for the first quarter.

Revenue rose 11.9% year over year to $124.3 million, but the result was dominated by a $14.46 billion unrealized loss on digital assets under fair-value accounting.

That outcome confirms the central tension around Strategy’s model. The company can show rising Bitcoin-per-share metrics while its reported earnings are reshaped by the market price of a single volatile asset.

Saylor’s preferred scorecard shows a company accumulating Bitcoin faster than dilution erodes shareholder exposure. Traditional accounting shows a business whose bottom line can swing by billions of dollars in a single quarter.

Bitcoin yield becomes Saylor’s main scorecard

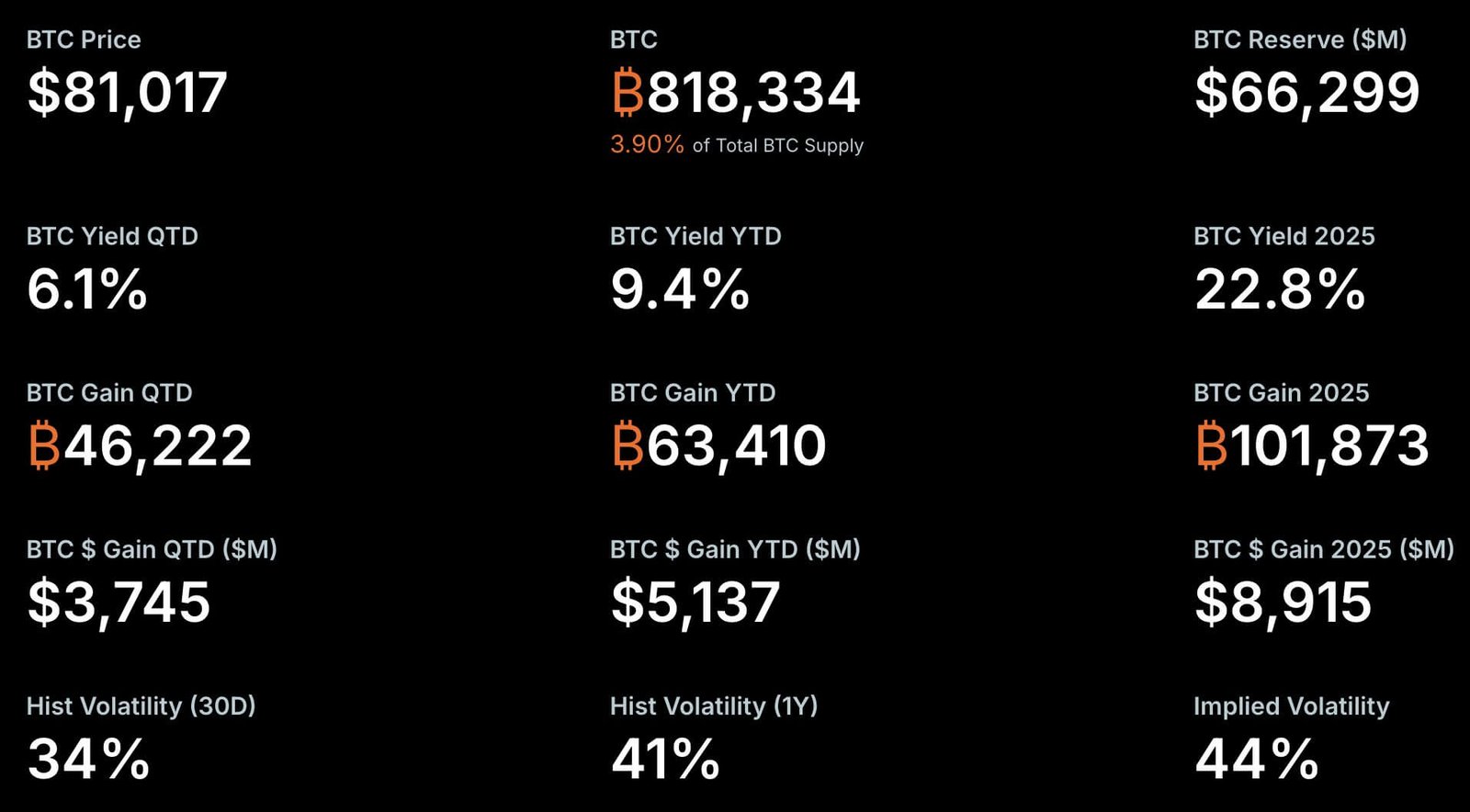

Strategy said its BTC Yield reached 9.4% year to date. The metric measures the change in Bitcoin holdings per diluted share, providing a way to assess whether the company is increasing Bitcoin exposure for shareholders even as it issues securities to fund purchases.

BTC Gain takes that percentage and turns it into a Bitcoin number. By Strategy’s calculation, the year-to-date increase equals 63,410 BTC.

The company also reported BTC $ Gain of $4.97 billion, a dollar-denominated version of the same internal measure.

For Saylor and his supporters, the figures are evidence that the company’s capital markets strategy is still producing incremental Bitcoin exposure for shareholders.

However, the measure is narrower than earnings, cash flow, or net income. It does not show whether Strategy’s software business is improving, whether dividend obligations are becoming harder to service, or whether the company’s financing costs are rising.

Instead, it answers one specific question: whether the company has increased Bitcoin per share over a selected period.

That distinction now frames the Q1 result. Strategy’s revenue came in at $124.3 million, up from $111.1 million a year earlier, leaving the legacy software unit in the background.

The bottom line was driven by Bitcoin accounting rather than product sales.

Strategy reported an operating loss of $14.47 billion, almost entirely due to the unrealized digital asset loss recorded during the quarter.

That creates a split between economic exposure and reported earnings. Strategy’s Bitcoin metrics improved, but common shareholders absorbed a GAAP loss far deeper than pre-earnings consensus estimates.

Bitcoin buying continued through the drawdown

The first quarter was a stress test for Strategy’s playbook. Bitcoin fell sharply during the period, yet the company continued to buy Bitcoin.

Strategy ended the period with 818,334 BTC as of May 3, representing a 22% year-to-date increase in holdings.

The company said its Bitcoin position had a market value of $64.14 billion as of May 1, based on a Bitcoin price of $78,374. Its average purchase price was $75,537 per coin, leaving the position modestly above cost at that reference price.

The holdings amount to about 3.9% of Bitcoin’s fixed 21 million token supply, giving Strategy a scale unmatched by any other public company.

That concentration is the source of both the appeal and the risk.

When Bitcoin rises, Strategy’s balance sheet expands quickly, and its stock can move with greater force than the token itself. When Bitcoin falls, the same leverage becomes a liability, creating accounting losses, pressure on the share price, and questions about whether the company should continue raising capital.

The stock’s history shows the size of that swing. Since Strategy began its Bitcoin transformation in 2020, MSTR shares have risen to as high as $500 in 2024, thanks to BTC’s rapid rise during the period, but have fallen to as low as $100 earlier this year amid the top crypto’s price struggles.

The post-earnings reaction showed how sensitive the equity remains to that balance. Strategy shares slipped after the results, even though the company continued to report growth in Bitcoin exposure.

That market response matters for Strategy’s model. A stronger share price can make equity issuance more attractive, while tighter credit markets or a falling stock can make capital raising more expensive.

Saylor’s strategy depends on Bitcoin’s long-term price and the market’s willingness to keep funding the company along the way.

Preferred stock becomes the new funding channel

Strategy’s financing structure has grown more complex as its Bitcoin holdings have expanded. The company has used convertible debt and common stock for years, but its preferred-stock program has become a more prominent part of the machinery.

STRC, Strategy’s variable-rate perpetual preferred stock, has become the clearest example. The instrument gives investors a high cash payout while giving Strategy another route to raise funds for Bitcoin purchases. It also broadens the buyer base beyond investors who want direct exposure to common equity.

Strategy said STRC raised $5.58 billion and had grown 189% year to date.

The preferred stock launched with a 9% annual dividend and has since moved higher after a series of increases designed to keep the instrument trading near par.

Strategy has also proposed a shareholder vote to double the STRC dividend payment frequency from monthly to semi-monthly, a change that would make the product look more like a regular income instrument for yield-focused investors.

The growth has been rapid. Saylor said STRC had scaled to $8.5 billion in market capitalization within nine months of launch, making it one of the company’s most closely watched securities.

It has also started to move beyond traditional markets. Strategy said $270 million of STRC was held across DeFi protocols, including Apyx and Saturn, while another $150 million was held in corporate treasuries.

Chief Executive Officer Phong Le has described STRC as a kind of battery that stores Bitcoin gains and distributes them over time.

The description reflects Strategy’s pitch: Investors in preferred stock receive income, while the company uses the capital to accumulate Bitcoin that could appreciate over the long run.

The structure works best when Bitcoin rises, Strategy’s common stock holds a premium, and investors remain eager to buy the company’s securities.

In that environment, new issuance can fund more Bitcoin purchases, thereby increasing BTC per share and supporting the broader valuation story.

Dividend burden raises the risk bar

The challenge is that Bitcoin does not produce income. Strategy’s software business still generates revenue, but it is small relative to the size of the company’s Bitcoin holdings and the obligations tied to its financing stack.

That makes the preferred dividend burden a central risk. As Strategy issues more preferred shares, its annual cash obligations rise.

Strategy reported $692.5 million in cumulative preferred dividends and distributions as of the first quarter. It also said it had more than $13.5 billion of preferred equity outstanding.

Those payments must be funded through existing cash, operating income, asset sales, or additional capital raising. The more the company leans on preferred stock, the more important market access becomes.

Strategy reported $2.21 billion in cash and cash equivalents at the end of the quarter, giving it liquidity against near-term obligations but leaving the broader model dependent on continued access to capital markets.

The company argues that its securities are supported by a large Bitcoin reserve. That is true in an economic sense, but the legal structure is more complicated.

STRC is unsecured, meaning holders do not have a direct claim on specific Bitcoin collateral. In a stress scenario, the order of claims across convertibles, preferred shares, and common equity would become critical.

The size of Strategy’s Bitcoin position also creates a market-structure issue. A forced sale by the world’s largest corporate Bitcoin holder would likely affect the price of the asset it is trying to monetize.

That makes the headline value of the holdings different from the amount that could be realized quickly under pressure.

For common shareholders, the risk is subordination. Preferred dividends sit ahead of common equity. If payments are missed, cumulative obligations can build rather than disappear, increasing the claim of senior securities on future value.

That does not mean the model is close to breaking. It means the cost of maintaining it rises as the company scales. Each new financing round can increase Bitcoin holdings, but it can also add obligations that must be serviced before common shareholders benefit.

The Q1 report narrowed the issue. Strategy’s Bitcoin scorecard improved, but its GAAP loss showed how sharply earnings can move against common shareholders when Bitcoin falls.

The next test is whether investors continue to fund that trade after a quarter in which the company reported nearly $5 billion in BTC gain and a $12.77 billion loss attributable to common stockholders.