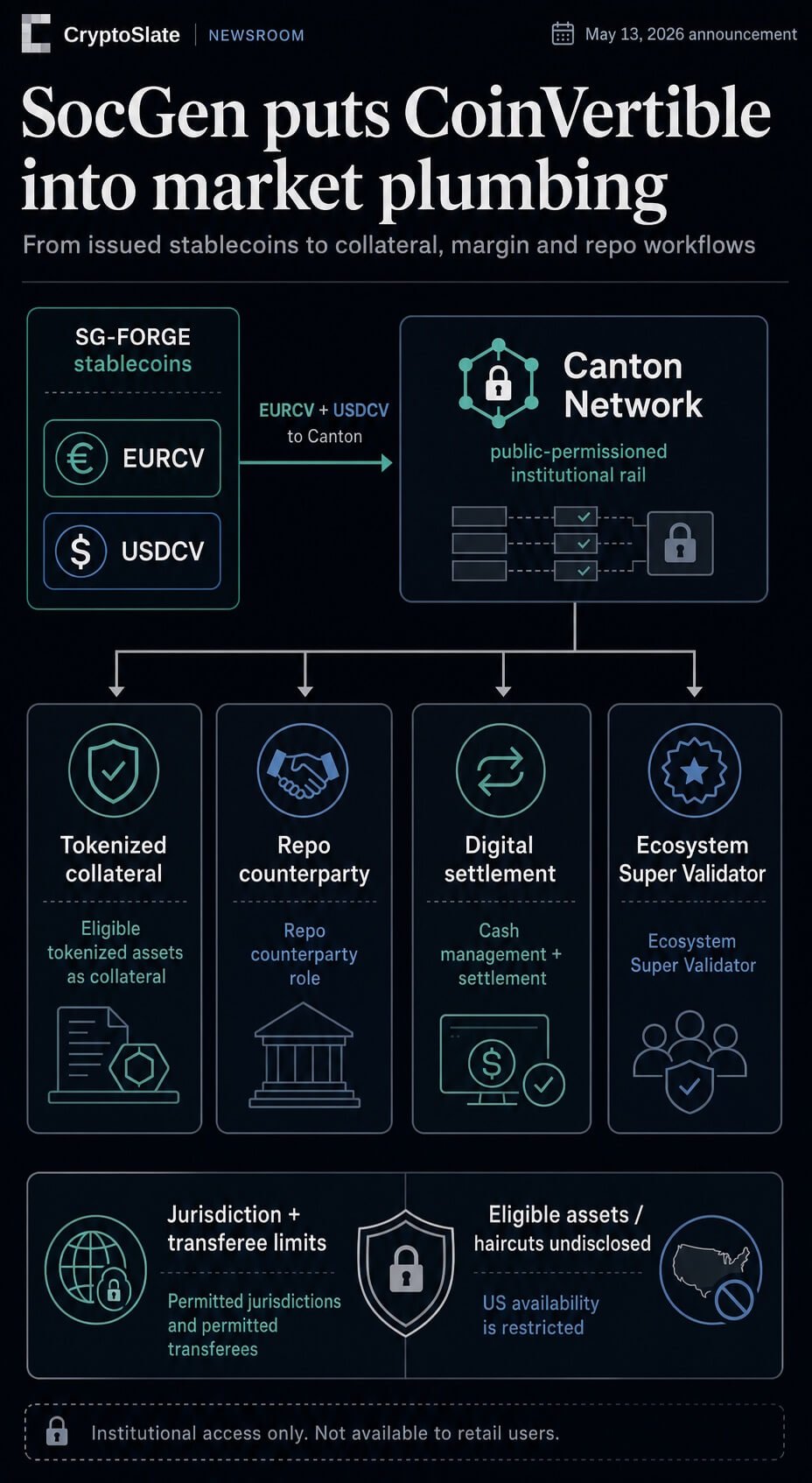

Societe Generale plans to bring SG-FORGE’s EUR CoinVertible and USD CoinVertible to Canton Network as part of a push into collateral, repo financing, and settlement.

The May 13 move puts the French bank’s stablecoin effort closer to the operating layer of institutional markets.

SG-FORGE has already issued regulated CoinVertible tokens, and CryptoSlate has covered the bank’s push into dollar and euro stablecoins. The Canton announcement connects those tokens to the market plumbing where collateral eligibility, margin calls, repo counterparties, settlement controls, and privacy requirements decide whether tokenized finance can move beyond isolated issuance.

In a May 13 statementSociete Generale said it is accelerating institutional blockchain-based financial infrastructure on Canton through its digital asset subsidiary. The bank said the work will focus on tokenized collateral, on-chain financing, and institutional-grade digital settlement.

It also plans to accept certain tokenized assets as eligible collateral, act as a counterparty in repo transactions, deploy USD and EUR CoinVertible on Canton, and join the network as an Ecosystem Super Validator.

That framing separates the announcement from a routine chain deployment. A stablecoin can trade on several networks without changing much about institutional finance.

A bank-issued settlement asset within a collateral and repo workflow is a different proposition because the token has to work within balance-sheet constraints, counterparty controls, jurisdictional limits, and risk systems that traditional finance already relies on.

| Announced capability | Intended market function | Known caveat |

|---|---|---|

| EURCV and USDCV on Canton | Settlement, cash management, and financing activity across tokenized markets | Limited to permitted jurisdictions and permitted transferees |

| Eligible tokenized collateral | Collateral mobility and operational efficiency for institutional clients | The eligible asset set and haircuts were not disclosed |

| Repo counterparty role | Support on-chain financing markets | The announcement leaves expected volumes and timing undisclosed |

| Ecosystem Super Validator participation | Support Canton’s institutional network operations | Validator status is infrastructure participation rather than recurring activity |

Market structure gives the move its context

Canton is already associated with institutional collateral and settlement tests rather than retail stablecoin distribution.

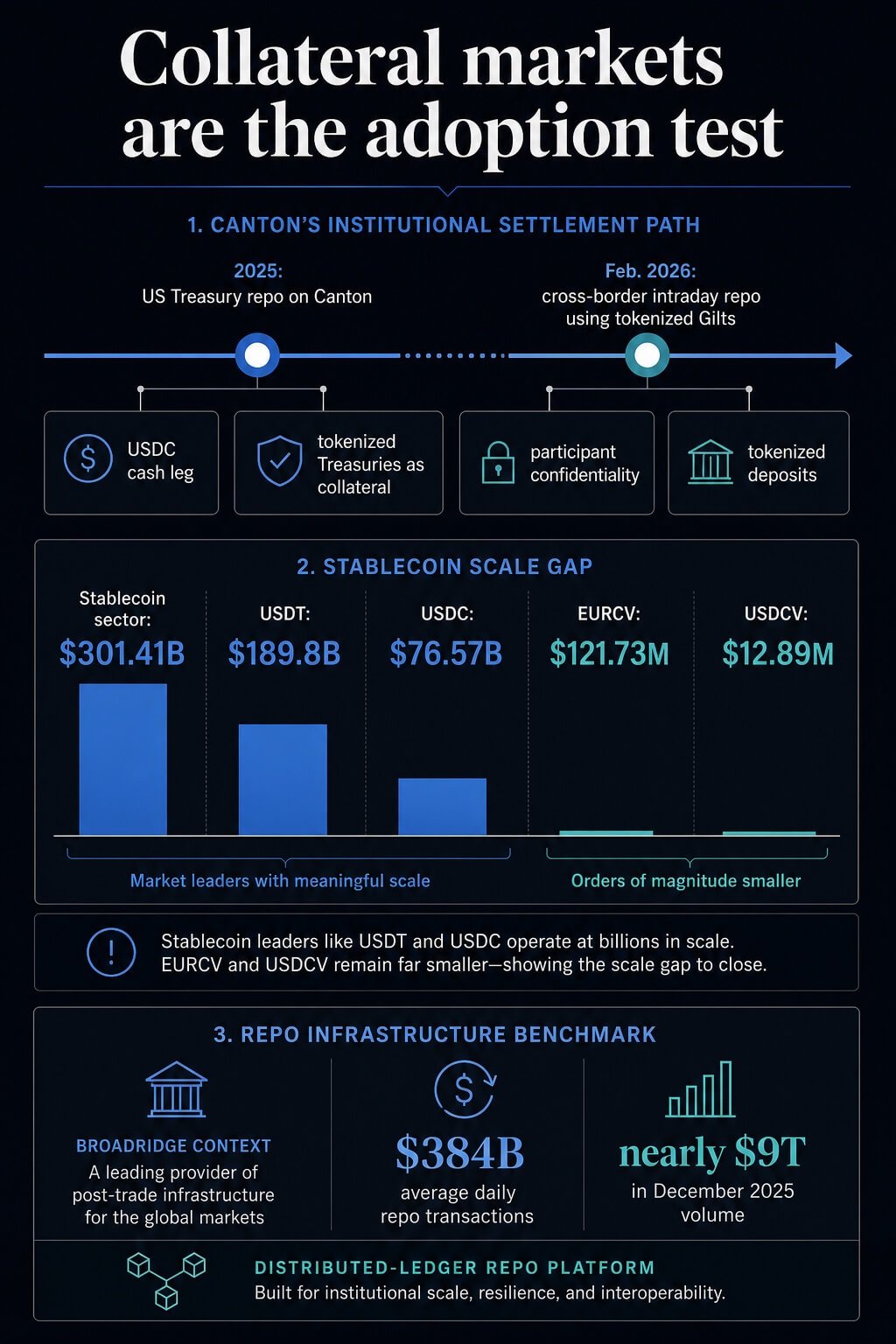

CryptoSlate reported in 2025 that Digital Asset and a consortium of major financial institutions completed an on-chain US Treasury repo transaction on Canton, using USDC as the cash leg and tokenized Treasuries as collateral.

That earlier trade was executed on Tradeweb during a weekend and positioned as atomic settlement of both legs on-chain within a public-permissioned institutional network.

Participants included Bank of America, Citadel Securities, Societe Generale, Virtu Financial, DTCC, Circle, Cumberland DRW, and Tradeweb, among others. The transaction showed how cash and collateral could be represented on the same institutional settlement rail, with participant confidentiality and established market venues still in view.

Canton’s working group added more collateral context in February 2026, when it reported cross-border intraday repo transactions using tokenized Gilts, including a cross-currency repo using tokenized Gilts against non-GBP tokenized deposits.

Société Générale was listed among the participants in that set of transactions as well. Thus, Societe Generale’s latest announcement reads as a follow-through on a specific market structure problem.

Institutions want faster collateral mobility and settlement outside legacy time windows, but they also need configurable privacy, permissioned access, legal restrictions, and operational controls. Canton is built around that tension, and Societe Generale is now putting its own regulated stablecoin product into the same conversation.

Super Validator participation adds another layer to that positioning.

The role signals that Societe Generale wants to support network infrastructure while building applications around collateral mobility, margin management, repo financing, and tokenized settlement. That still leaves the commercial question open, but it places the bank closer to the systems that would validate, synchronize, and govern institutional transactions if the workflow moves from tests into regular use.

Regulation comes before scale

SG-FORGE’s CoinVertible product gives the announcement its bank-led settlement angle.

The CoinVertible page describes USD CoinVertible and EUR CoinVertible as fiat-pegged tokens backed by segregated collateral assets, with direct subscriptions available after SG-FORGE onboarding and broader access through exchanges, brokers, and market makers.

The page also says SG-FORGE is a regulated electronic money issuer, investment firm, and crypto-asset service provider.

The regulatory status is supported by the French AMF’s white-list entrywhich lists SG-FORGE as a MiCA-licensed crypto-asset services provider in France.

CryptoSlate previously reported that USDCV launched in 2025 as SG-FORGE’s dollar-pegged stablecoin on Ethereum and Solanawith BNY Mellon as reserve custodian and daily reserve disclosure language tied to MiCA transparency standards.

Institutional cash legs cannot simply be liquid. They also need issuer controls, redemption rules, reserve clarity, and transfer restrictions that fit the venue and the counterparty.

The same features that make a stablecoin less open-ended for general crypto users can make it more usable inside permitted institutional workflows.

The limits are just as important.

SG-FORGE’s Canton announcement says EURCV and USDCV are unregistered under the US Securities Act and restricted from offers, sales, pledges, or transfers outside of offshore transactions to permitted transferees. It also says SG-FORGE lacks a license or authorization to conduct business in the United States.

That language should prevent any reading that the Canton deployment creates broad US retail availability.

Scale also remains a constraint.

CryptoSlate’s stablecoin sector data shows a market capitalization of about $301.41 billion, with Tether’s USDT at around $189.8 billion and USDC at $76.57 billion.

By comparison, CryptoSlate’s pages for EURCV and USDCV showed about $121.73 million and $12.89 million in market capitalization, respectively.

CoinVertible may be designed for bank-grade settlement, but a small circulating base means any meaningful financing market would still need issuance, counterparties, liquidity channels, and actual transaction demand.

The real test is repeatable repo activity

Societe Generale’s announcement arrives as other market infrastructure firms are also trying to move collateral and repo workflows onto distributed ledgers.

Separate from Canton and SG-FORGE, Broadridge said in January that its Distributed Ledger Repo platform processed an average of $384 billion in daily repo transactions in December 2025, with total volumes of nearly $9 trillion for the month.

That context establishes repo as a live institutional target for tokenized settlement infrastructure, while leaving Canton and CoinVertible demand to be proven on their own terms.

The question for Societe Generale is whether its Canton role turns into repeated institutional financing activity.

The bank said it plans to accept certain tokenized assets as collateral and act as a repo counterparty, but it left asset eligibility, haircuts, CoinVertible deployment timing, and client activity expectations undisclosed.

Those omissions are common in an early infrastructure announcement, but they define the next phase of scrutiny.

If Societe Generale can use Canton to support recurring collateral, margin, and financing flows, CoinVertible becomes more than just a bank-issued stablecoin seeking distribution. It becomes a controlled settlement asset inside a specific institutional market workflow.

If activity remains limited to controlled tests, the announcement will look more like another high-profile tokenization milestone: strategically coherent, technically relevant, and still short of proving that on-chain collateral markets have durable demand.

Societe Generale’s Canton move is a concrete step toward regulated stablecoins serving collateral and repo settlement infrastructure. The evidence still points to early-stage activity rather than broad adoption.

The signal to watch is whether the bank turns Super Validator participation, eligible tokenized collateral, and CoinVertible settlement into repeated financing activity with named counterparties, disclosed limits, and observable market use.