Last week, an institutional investor executed the largest single off-exchange trade in the history of US spot Bitcoin exchange-traded funds, offloading a $1.26 billion position in BlackRock’s iShares Bitcoin Trust (IBIT).

While the transaction has sparked intense debate on Wall Street, an analysis from NEEDFUL suggests the sale was a targeted, urgent retreat by a whale rather than the routine closure of a popular hedge fund arbitrage play.

According to the analysis, the entity paid a steep price for immediate liquidity. It incurred nearly $30 million in execution costs just to secure an exit before the broader digital asset market took a notable downturn.

Understanding the IBIT megatrade

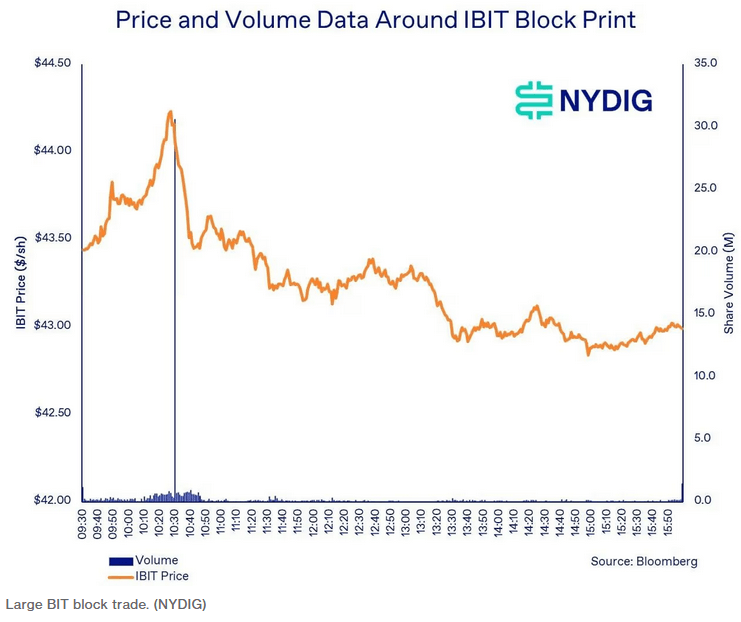

NYDIG noted that activity in BlackRock’s IBIT began to quietly accelerate following an early-morning session with normal volume.

According to the firm, the ETF’s share price edged upward from $43.81 to an intraday peak of $44.24 between 10:16 a.m. and 10:28 a.m. Eastern Time. Trading volume during this window surged to three or four times its normal rate, suggesting an executing broker was testing market liquidity and carefully priming the tape for a massive placement.

Then, at precisely 10:30 a.m., the hammer fell.

A single seller dumped 29.21 million shares of IBIT in a privately negotiated, off-exchange transaction. The block cleared at $43.16 a share. Because the prevailing open-market price at that very second was $44.17, the seller accepted a 2.3% haircut on the spot. In dollar terms, that execution penalty cost the mysterious entity roughly $29.5 million.

Regulatory reporting codes attached to the trade illustrate the seller’s singular focus on speed. The transaction was printed to the FINRA/Nasdaq TRF Carteret, which is a facility used by broker-dealers to report dark pool and privately negotiated trades.

Furthermore, it carried an Intermarket Sweep Order designation alongside a Reg NMS trade-through exemption.

In plain English, these exemptions allow institutional players to bypass the requirement of seeking the absolute best displayed price across multiple public exchanges, provided they take responsibility for satisfying certain protected quotes.

This shows that the seller actively chose the certainty of an instant, unified exit over the possibility of a better price.

Debunking the arbitrage myth

When highly unusual, billion-dollar prints occur in crypto ETFs, market commentators typically default to a common explanation: the basis trade.

This popular hedge fund strategy involves buying a spot ETF while simultaneously shorting Bitcoin futures to harvest the yield from the price spread between the two.

However, NYDIG’s analysis identifies three distinct factors that dismantle the basis-unwind theory in this instance.

First, the basic economics do not align. A basis trader relies on capturing a narrow percentage yield over time. Accepting an immediate 230-basis-point loss on the spot leg of the trade would instantly vaporize a massive portion of the strategy’s anticipated annual return.

Unless facing a catastrophic margin call, an arbitrage desk would naturally unwind its position passively over days or weeks to preserve capital.

Second, the trade’s structural urgency is entirely misaligned with delta-neutral management. Intermarket sweep orders and hefty block discounts are the hallmarks of a distressed or deeply convicted directional seller, not a market-neutral yield farmer.

Finally, the futures market provided the ultimate smoking gun. A 29.21 million-share block in IBIT equates to roughly 18,500 Bitcoin. If an arbitrageur were exiting a delta-neutral position of that magnitude, they would need to simultaneously buy back roughly 3,700 Bitcoin futures contracts on the Chicago Mercantile Exchange (CME) to flatten their book.

However, the CME order book barely registered a pulse on the day. During the exact minute the ETF block crossed the tape, only 91 futures contracts changed hands. Over the entire half-hour window surrounding the trade, barely 1,000 contracts were executed.

Moreover, a true basis unwind of this size would have required absorbing nearly half of the CME’s total daily volume in an instant, which would have triggered a massive, highly visible spike in futures activity.

So, the total absence of such a spike confirms the seller was simply long on Bitcoin and suddenly wanted out.

Who is the whale?

The sheer scale of the transaction leaves a remarkably short list of suspects.

NYDIG noted that the block trade exceeded the total holdings of all disclosed 13F investors in the first quarter of 2026, excluding authorized participants and market makers, who hold inventory strictly for liquidity provision rather than investment purposes.

Following a trade of this magnitude, analysts naturally look to fund flows to track the aftermath. It will go recorded $192 million in net redemptions on May 26, followed by an additional $528 million on May 27.

However, market mechanics suggest these figures do not represent the direct, immediate settlement of the whale’s shares.

Because the ETF’s net asset value closed at $42.95 on the day of the trade and at $42.43 the following day, which is well below the negotiated $43.16 block-execution price, the counterparty that purchased the shares had no economic incentive to immediately redeem them with the issuer.

Doing so would have locked in an instant loss. Instead, the buyer likely absorbed the block into inventory and has been systematically distributing the shares into the secondary market over time.

So, the ultimate identity of the seller and their motive remain shrouded in the opacity of off-exchange trading. It is impossible to definitively prove whether the whale was forced out by strict internal risk limits or whether they made a discretionary bet that the crypto market was headed for a sustained downturn.

Market headwinds and institutional fatigue

Following the trade on May 26, Bloomberg ETF analyst Eric Balchunas claimed the “market absorbed the sale well.”

However, the timing of the billion-dollar retreat proved proactive, as May was a bruising month for digital assets. Data from CoinGlass showed that the top crypto shed nearly 4% over the month, trading near $73,000 at the end.

This price performance was exacerbated by the collapse in investor appetite for spot Bitcoin ETFs.

NYDIG noted that the US funds entered the May 26 session already nursing a six-day streak of consecutive outflows. The sector bled $1.55 billion during that stretch alone, with BlackRock’s IBIT shouldering the brunt of the damage, shedding roughly $1.1 billion.

By the close of May, the damage had compounded. The US-listed spot Bitcoin ETFs hemorrhaged $2.4 billion in total monthly outflows, according to data from SoSoValue.

The sustained selling pressure dragged total assets under management across the ETF category from north of $100 billion down to $94.17 billion.